📊 Why People Are Moving to North Carolina, and What It Means for Fort Bragg & Moore County Real Estate

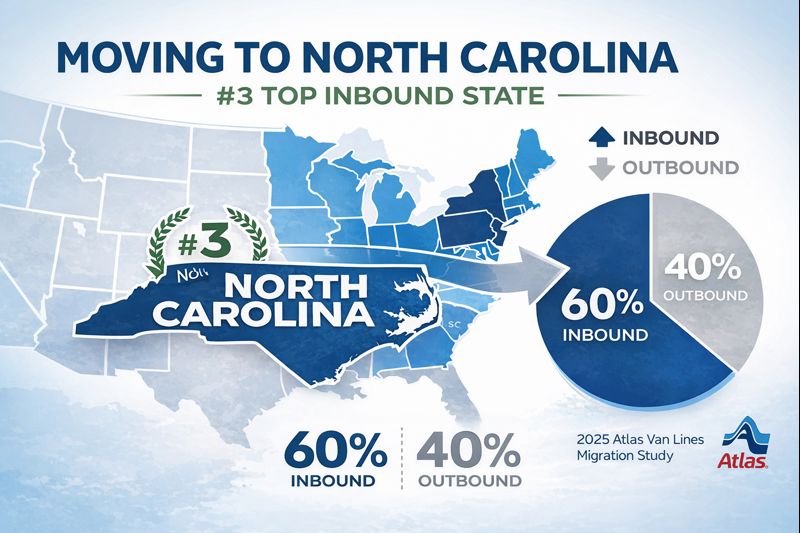

According to the 2025 Atlas Van Lines Migration Patterns Study, North Carolina ranks #3 in the nation for inbound moves, and that growth is being felt right here in Moore County and the Fort Bragg area.

At FTM Realty, we don’t just watch market trends, we live them. Every week, we're helping people relocate, transition, and plant new roots across Moore County and surrounding areas near Fort Bragg. If you’re thinking of making a move in 2026, you need local experts who’ve done this before.

🧭 Why North Carolina Is Booming: 2025 Inbound Migration Trends

Between November 2024 and October 2025, North Carolina saw 60.3% inbound moves, placing it third nationally.

Top 10 Inbound States (2025):

- Arkansas – 68.2%

- Idaho – 63.6%

- North Carolina – 60.3%

- Hawaii – 60.0%

- Washington, D.C. – 59.0%

- Tennessee – 57.3%

- Washington – 56.9%

- Alabama – 56.8%

- North Dakota – 56.1%

- New Hampshire – 55.0%

The message is clear: People are choosing NC for affordability, quality of life, job growth, and lifestyle opportunities, and the impact is being felt right here in Vass, Southern Pines, Pinehurst, Sanford, Fayetteville, and beyond.

🏡 Why Moore County, NC and Fort Bragg NC Surrounding Areas Are on Their Radar

The Atlas study points to several key factors that continue to shape where people relocate:

📌 Affordability Constraints

Many parts of the U.S. remain costly for homeownership. States with more affordable housing and taxes, like North Carolina, become magnets for buyers.

👨👩👧 Lifestyle Priorities

People want:

- family‑friendly communities

- access to outdoor living and green space

- good schools, lower cost of living, and balanced pace of life

Moore County and the Fort Bragg areas deliver on all of these fronts, and buyers are taking notice.

As inbound moves surge, Moore County and surrounding counties (Lee, Harnett, Hoke, and Cumberland) adjoining Fort Bragg stands out as a prime destination for:

- Military relocations (we’re just outside Fort Bragg)

- Families looking for space, schools, and community

- Retirees drawn to golf culture in Pinehurst and the Sandhills and charm

- Many areas are commutable to the Raleigh Durham Research Triangle area, one of the largest growing areas where businesses are relocating from higher taxed stats.

- Remote workers escaping urban pressure for peaceful living

📍 What This Means for Buyers & Sellers

As inbound migration continues to shape the real estate market across Moore, Harnett, Lee, Hoke, and Cumberland Counties, here’s how it’s impacting both sides of the transaction:

🏡 For Buyers

✔ Increased competition in select neighborhoods

✔ More buyers relocating from out-of-state markets

✔ Continued demand for well-priced resale homes

✔ Higher search activity near jobs, schools, and military bases

📈 For Sellers

✔ Inbound buyers = serious demand

✔ Homes priced and marketed correctly are still selling

✔ Out-of-state cash and 1031 exchange buyers are actively circling

✔ The right agent positions your home for maximum exposure and results

🧠 Bottom Line

North Carolina’s inbound migration trend isn’t just data, it’s real people choosing this community for their next chapter. And this continued growth is bringing buyers, opportunities, and momentum to our local housing market.

If you’re thinking about buying, selling, or relocating to Moore County, you should have a trusted local expert in your corner.

✨ Let’s Build Your Next Chapter Together

With:

✔ Over 30 years of combined military service

✔ 18+ years of combined real estate experience

✔ Hundreds of relocations managed in Moore County and surrounding areas

…we bring confidence, clarity, and results to every move.

Whether you’re:

- moving across state lines,

- relocating due to military orders,

- upsizing, downsizing, or investing,

We’re here to help you make the smartest move possible.

🎯 Not ready to move yet?

Browse for homes on our fully MLS indexed and updated website or stay in the know with our local market updates—see what homes are selling for near you.

🏡 Curious what your home’s worth today?

Get real-time insights with our free Homebot tool—track your home value, equity, and personalized market trends, all in one place.

📞 Want expert guidance tailored to you?

Call us at 910.585.5772, visit www.FTMRealty.com, or book a quick call on our calendar to start the conversation.

Frank Murphy is a licensed North Carolina Realtor and Broker/co-owner of Frank & Tracy Murphy, LLC (FTM Realty), a husband-and-wife brokerage built on service, experience, and results. Together, Frank and Tracy specialize in military relocation and residential real estate throughout Fort Bragg and surrounding communities, including: Southern Pines, Pinehurst, Vass, Fayetteville, Sanford, and Raleigh. They proudly serve Moore, Harnett, Lee, Hoke, Cumberland, and neighboring counties within a 40-mile radius of Fort Bragg, helping clients make smart, stress-free moves with trusted guidance every step of the way.

---

📍 **Frank & Tracy Murphy, LLC (FTM Realty)**

PO Box 310, Vass, NC 28394

📞 910.585.5772

📧 FrankandTracyMurphy@gmail.com